We hope you and your loved ones found time to break bread and share stories from 2023 over the Christmas season. In keeping with our Year-in-Review tradition, we’ve reflected and compiled our thoughts on the events of last year. Highlights of this edition include: banking crisis, wars, wildfires, record low personal savings, record high credit, magnificent seven, falling inflation, political nonsense, Swift, Kelce, and Modelo.

Business

Banking is big business. When big business booms, the world operates as usual. When it fails, panic ensues. Silicon Valley Bank (SVB) found itself in the spotlight in the first half of 2023. Banks aren’t in the business of holding your money; they’re in the business of making their own. In the spirit of simplicity, SVB wagered interest rate increases wouldn’t occur. Well, they did. Bond prices and interest rates have an inverse relationship. In March, SVB attempted to purchase more attractively priced bonds due to interest rate increases (bonds went on sale), and in doing so, sold bonds they owned for a loss of $1.8 billion. Depositors took note, came to collect (almost $50 billion in one day), and SVB didn’t have the reserves on hand to fulfill depositors’ demands – enter government safety net, but not before panic and uncertainty rippled through the industry. The result: government bailout and, for some, decreased trust in the banking sector.

2023 brought with it banking failure, but also marketing failure. Jennifer Maloney, a reporter for the Wall Street Journal, follows trends across business landscapes. Last year, she wrote several pieces related specifically to a household name – Bud Light. Bud Light’s marketing team sparked a boycott by partnering with a transgender influencer early in the year. A special Bud Light can with Dylan Mulvaney’s face was advertised online – big mistake. The marketing effort wasn’t well received. The bottom-line: sales decreased dramatically and a competitor, Modelo Especial, claimed the number one spot as a top-selling U.S. beer by dollar sales in retail stores. What is the old saying? One man’s trash is another man’s treasure? Cheers, Modelo.[1]

Politics & the World

The war in Ukraine continued. Russian aggression doesn’t seem to be slowing, nor does our aid to Ukraine. According to an article from the Council on Foreign Relations, the U.S. has supplied over $70 billion of aid to Ukraine since January 2022. As of last summer, Ukrainian pilots began training to fly U.S.-made F-16s.[2]

In October, the Iran-backed terrorist group Hamas attacked multiple Israeli cities on the border of Gaza, killing and injuring thousands of Israelis and taking hundreds hostage. Hamas has controlled the Gaza strip since 2006 – the result of their victory in the Palestinian Authority’s parliamentary election. Waves of violence ensued in the region, particularly highlighted by machine guns, rockets, and bombs. Like the war between Russia and Ukraine, the U.S. is involved (at least monetarily) and this conflict doesn’t seem to be slowing either.[3]

The political landscape in the U.S. was nothing short of interesting last year. In addition to our government avoiding shutdown by way of continuing resolution, the House gained a new speaker, Mike Johnson (Louisiana). Johnson is the 56th Speaker of the House and has his roots deeply situated in faith. If positivity is to come from our government, faith is an ideal starting position.

The Pew Research Center conducted a study showing President Joe Biden receives disapproval from almost two-thirds of Americans. Sixty-four percent of people aren’t confident that President Biden can make good decisions about economic policy. Seventy-five percent of Americans aren’t confident that President Biden can bring the country closer together. I’m sure Biden isn’t liking his numbers right about now.[4]

Sports

The Women’s World Cup was held in Australia and New Zealand in 2023. Historically, the U.S. women’s performance in the World Cup is stellar. With victories in 1991, 1999, 2015, and 2019, the bar is firmly situated at the top. Remember, this tournament is played once every four years, making each victory more impressive. This year we lost in the round of 16. Spain was crowned champion.

To remark further on Spanish excellence, Jon Rahm etched his name in the history books as he became the fourth Spaniard to win the Masters. He beat Brooks Koepka and Phil Mickelson by four strokes. To close his 2023 season, Rahm agreed to a $400 million deal to join the LIV Tour.

This wouldn’t be much of a Year in Review if Taylor Swift and Travis Kelce didn’t have their names attached to the sports section. These two don’t need introductions, but if you have watched a Kansas City Chief’s game during the 23/24 season, you have seen more of Taylor Swift than any of the football game. She isn’t on the roster, but never ever ever, say never.

FED and Macro

The FED had a busy 2023. Jerome Powell and company found themselves center stage again last year. Inflation data (commonly tracked using the Consumer Price Index) began the year up 6.34% from January 2022. The FED used one of the tools in their monetary policy chest (interest rates) four times in 2023. The February, March, May, and July FED meetings all resulted in 25 basis point rate increases. Headline CPI data has continued to fall from January highs, but headline data doesn’t tell the whole story. Energy has driven headline CPI down tremendously this year, but items like rent, nonprescription drugs, motor vehicle maintenance and repair, lodging away from home, admission to sporting events, food at employee sites and schools, and medical equipment and supplies all remain well above the headline number. Spend money on any of these? In the last couple weeks, several articles in the Wall Street Journal contained inquiries about why the consumer is so doom and gloom: unemployment is low, inflation is falling, hourly earnings have surpassed headline inflation. Well, if you read beyond the headlines and do a little homework, the categories listed above are “big ticket” items and weigh heavily on consumer wallets.

| Month | Interest Rate Increase | CPI % Change | Hourly Earnings % Change |

| January | – | 6.34 % | 4.39 % |

| February | + 25 BP | 5.98 % | 4.67 % |

| March | + 25 BP | 4.98 % | 4.30 % |

| April | – | 4.95 % | 4.38 % |

| May | + 25 BP | 4.12 % | 4.33 % |

| June | – | 3.09 % | 4.41 % |

| July | + 25 BP | 3.29 % | 4.33 % |

| August | – | 3.70 % | 4.28 % |

| September | – | 3.68 % | 4.24 % |

| October | – | 3.23 % | 4.04 % |

| November | – | 3.12 % | 3.96 % |

| December | – | TBD | TBD |

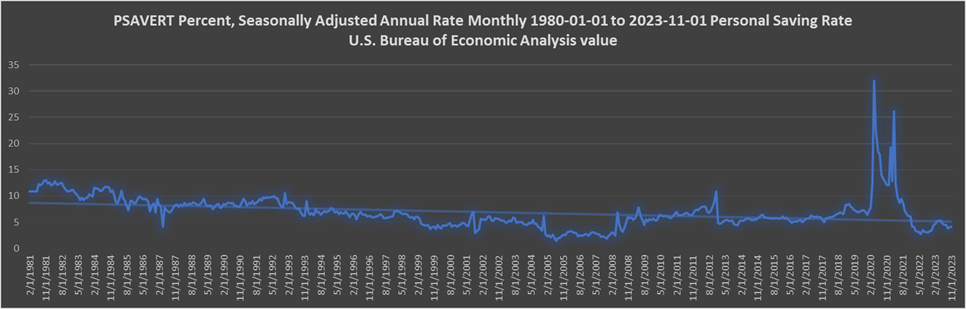

To obscure macroeconomic outlook further, the personal savings rate remains low. If we look at a trendline stretching more than 40 years (back to the 80s), the slope is negative. Simply stated, people are saving less. Notice the trend below:

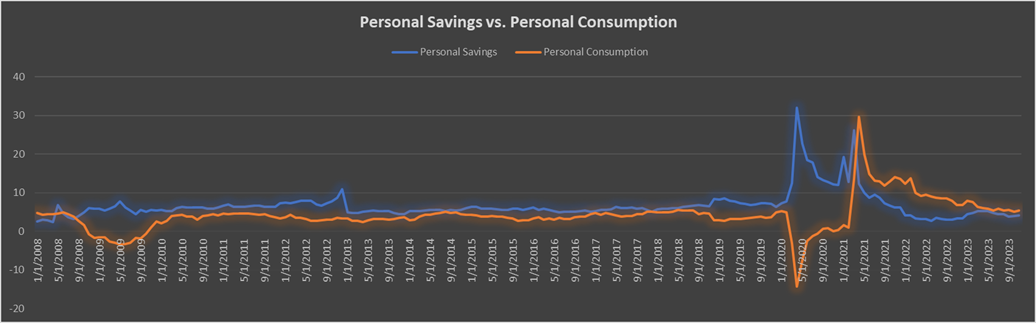

Additionally, people are spending more than they did in the past. Rather than looking at a 40-year period, let’s look at a chart with data from 2008. The average personal consumption rate between January 1, 2008 and January 1, 2020 was 3.33%. Since January 1, 2022, the average personal consumption rate has been 7.70%. Since early 2021, the personal savings rate and personal consumption rates have been inverted. There was significant variance in consumption and savings during the COVID-19 pandemic, but we can’t be sure we have felt the effects of this inversion.

Market

Battered and bruised in 2022, the major indices rebounded in 2023. Below is a look at the three major indices performances across 2022 and 2023.

- Dow Jones: -8.78% in 2022; Began the year at $36,338 and ended the year at $33,147.

- Dow Jones: +13.7% as of 12/29/2023; Closed at $37,689.54

- S&P 500: -19.44% in 2022; Began the year at $4,766 and ended the year at $3,839.

- S&P 500: +24.23% as of 12/29/2023; Closed at $4,769.83.

- Nasdaq: -33.10% in 2022; Began the year at $15,644 and ended the year at $10,466.

- Nasdaq:+43% as of 12/29/2023; Began the year at $10,466.48 and ended the year at $15,011.35.

It is easy to get caught up in the noise surrounding the markets. 2023 is a perfect example. The magnificent seven (Apple, Microsoft, Amazon, Alphabet, Meta, Tesla, and Nvidia) had a tremendous year. Several of these companies experienced triple-digit growth. Remove these from the equation and the story so many are singing today would have a different tune. If you bar the magnificent seven earnings from the S&P 500, aggregate earnings across the rest of the index are negative.[5]

Let’s say you had a passively managed portfolio of $1,000,000 to begin 2022 and invested it in the S&P 500 index. At the end of 2022, you would have been left with approximately $805,600 – and probably your stomach in your throat. In 2023, your funds are still invested in the S&P 500 Index. Your $805,600 likely grew by 24.23%. Congratulations! You end the year with approximately $1,000,796.88. You are up $796.88 after two years of full exposure to the market. Remember, the market is relative. Volatility is unavoidable, but it is manageable. You may have been up 24.23% this year, but how far did you fall the prior year?

Let’s do another experiment. Rather than a passively managed portfolio, you have an actively managed portfolio with downside protection understood as a core initiative. This isn’t related to annuities – this is pure portfolio management and strategic implementation of sophisticated strategies. The $1,000,000 portfolio at the beginning of 2022 is no longer exposed to the full risk of the market. Rather than a 19.44% decline, your $1,000,000 experiences a 4% decline. You now have approximately $960,000, and your stomach is where it’s supposed to be. By the end of 2023, rather than climbing 24%, your $960,000 experiences a 6% return. You end the year with approximately $1,017,600. You are up $17,600 after two years and didn’t experience a roller coaster of emotions or wild volatility in your accounts. Often, there is more than one way to get to your destination.

Thoughts for 2024

Interest rates remain elevated, and the economy continues to slow by most metrics. In our opinion, the possibility of recession is above 50% but we don’t believe it will be a deep, or long-lasting recession. Nevertheless, 2024 is setting up to be a year for volatility based on the forces at play. Many of the trends and themes prevalent in 2023 will extend well into 2024 – possibly beyond. With this in mind, we remind our clients that our strategy is to remain neutral as things play out. We also encourage you to reach out with questions. Our thoughts for 2024 are far more expansive than what is written here. You know how to contact us, and you know where to find us.

Sources

[1] https://www.wsj.com/business/the-bud-light-boycott-was-just-the-beginning-of-a-crazy-year-for-beer-9de3a402

[2] https://www.cfr.org/article/how-much-aid-has-us-sent-ukraine-here-are-six-charts

[3] https://www.cfr.org/global-conflict-tracker/conflict/israeli-palestinian-conflict

[4] https://www.pewresearch.org/politics/2023/12/14/assessments-of-joe-biden/

[5] https://www.wsj.com/finance/stocks/its-the-magnificent-sevens-market-the-other-stocks-are-just-living-in-it-5d212f95